Co-investment Primer

January 2026

There has been a notable surge in co-investment activity across the private markets, driven largely by the strategic mandates of major institutional players. This growth is primarily motivated by the opportunity to scale private market exposure while significantly reducing the aggregate cost of capital.

This primer provides a comprehensive overview of the co- investment mechanics, evaluating the specific advantages and operational hurdles inherent in the strategy. Furthermore, we outline the primary access points for investors and the critical factors involved in designing a robust co-investment program. Although the following analysis centers on private equity, these principles and structures are increasingly prevalent across the broader spectrum of private market asset classes.

Key Takeaways

Definition and Structure:

A co-investment occurs when a limited partner (LP) invests capital directly into a specific company alongside a general partner (GP). Such a structure differs from standard fund commitments because it removes “blind pool” risk, as the LP evaluates the specific asset and decides whether to commit capital on a case-by-case basis.

Benefits to LPs:

Co-investments provide several strategic advantages to LPs, most notably through reduced fee structures, more precise portfolio exposure, and the mitigation of the J-curve effect. Hence, providing LPs with more portfolio control and flexibility.

Performance:

Empirical research shows that the gross returns of co-investment deals generally track closely with the performance of assets held exclusively within a fund.1 Consequently, co- investments are expected to yield higher net performance, on average, than traditional fund commitments due to their more attractive economics (i.e., lower fees).

Considerations for LPs:

Engaging in co-investments requires a higher level of operational readiness. Investors must navigate highly compressed due diligence windows and maintain streamlined internal approval processes to meet GP timelines. Furthermore, concentration risk is a potential consideration; LPs must carefully manage the risk of over-exposure to any one company.

GPs’ Perspective:

GPs offer co-investment opportunities for several strategic reasons, such as securing supplemental capital for larger acquisitions, managing concentration risk within their fund, and retaining control over an investment. Additionally, providing these opportunities serves as a powerful tool for relationship management, deepening the alignment between the GP and their LPs.

1. Braun, Reiner and Jenkinson, Tim and Schemmerl, Christoph, Adverse Selection and the Performance of Private Equity Co-Investments (December 14, 2018). Available at SSRN: https://ssrn.com/abstract=2871458 or http://dx.doi.org/10.2139/ssrn.2871458

Understanding Co-investments

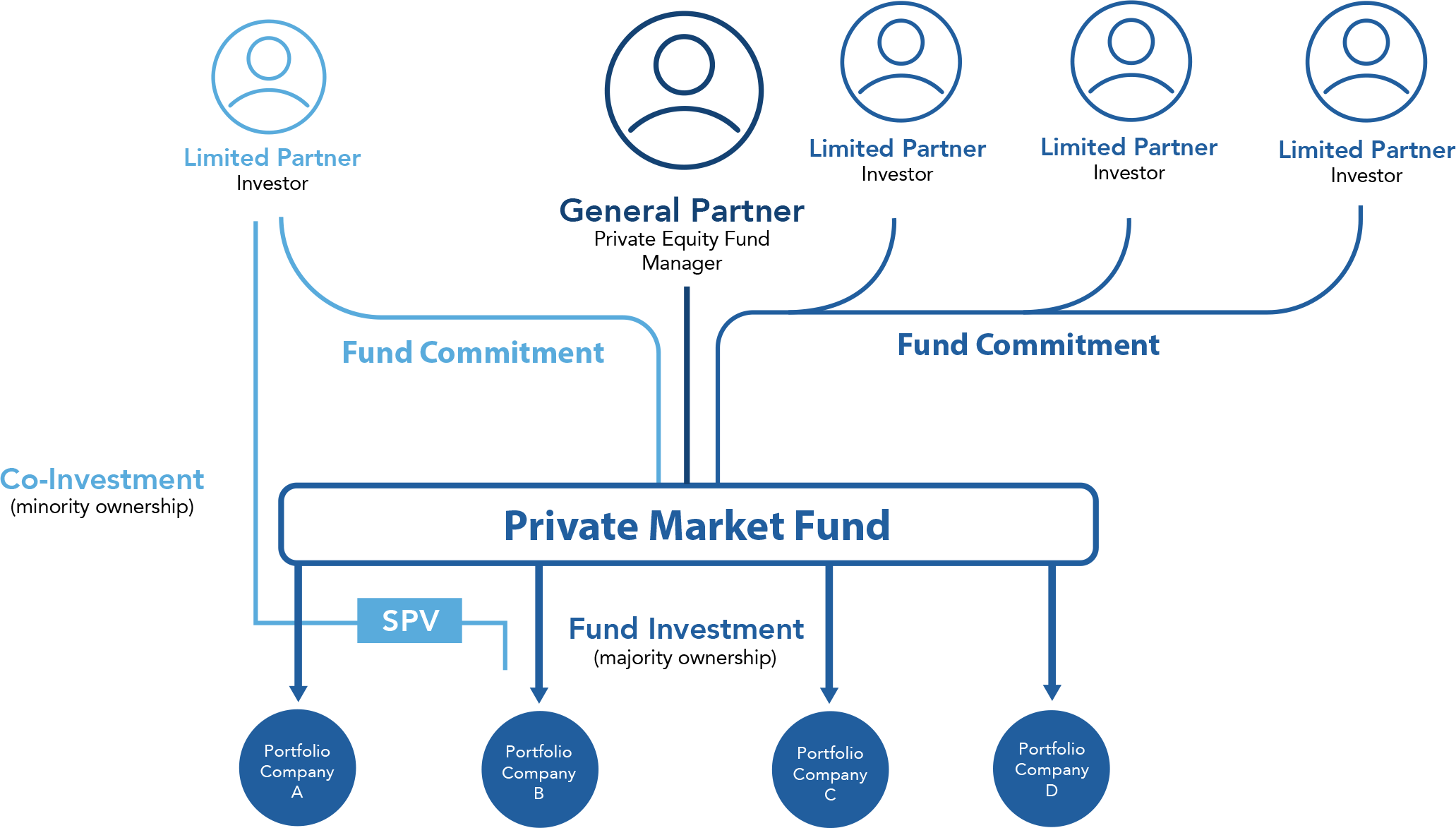

Private market investors generally construct the majority of their portfolios by committing capital to commingled, limited-life investment vehicles, commonly referred to as “funds,” raised periodically by General Partners (GPs). In such a structure, the Limited Partner (LP) is required to participate pro-rata in every transaction the GP executes for that specific fund. Because the individual assets are not identified at the time of the commitment, this traditional model is often described as a “blind pool.”

In contrast, a co-investment represents a more collaborative framework where an LP invests alongside a GP directly into a specific portfolio company being acquired for a fund. Most co-investors also hold an LP position in that underlying fund, effectively increasing their capital allocation to a deal they already have exposure to. However, this approach removes “blind pool” risk, as the LP retains participation discretion regarding any specific co-investment opportunity.

Co-investments are generally deployed into the same assets held by the main fund, typically resulting in the LP holding a minority equity stake in the underlying company. When aggregated with the holdings of the GP and other co-investors, these positions often represent a majority stake. The GP typically retains control over the strategic timing and method of the ultimate exit, governing both the main fund’s interest and the co- investment position. Figure 1 depicts a schematic for a typical co-investment.

Figure 1. Typical Co-investment Structure

Steps of a Co-investment

GPs typically begin the search for co-investors during the late stages of their due diligence process or shortly following the completion of a transaction.

Step 1: Initial Outreach

The GP selectively contacts LPs who have demonstrated interest in co-investment opportunities. During this phase, the GP provides a high-level summary of the transaction and solicits formal indications of interest.

Step 2: Information Exchange

Assuming interest, the GP grants access to comprehensive investment offering documents and a virtual “data room” containing due diligence materials related to the transaction.

Step 3: Direct Diligence

The GP may facilitate site visits or direct meetings between the LP and the portfolio company’s management team.

Step 4: Legal Finalization and Closing

The GP and LP negotiate the specific legal documentation governing the investment, leading to the formal closing of the co-investment capital.

GPs are aware that many LPs have developed sophisticated in-house capabilities to execute on these opportunities. Because co-investments are highly sought after, GPs generally offer them preferentially to existing LPs rather than seeking external capital. Most Limited Partnership Agreements (LPAs) grant the GP discretion in determining which co-investment opportunities are offered.

What Characteristics are Sought by GPs in a Co-investor?

General Partners prioritize specific characteristics when selecting Limited Partners for co-investment opportunities, notably decision-making speed, commitment size, and reliability. GPs frequently prioritize co-investment rights for LPs they identify as core strategic partners. Often, such partners are those who provide the largest capital commitments to an individual fund or across a series of funds managed by the firm. Large commitments suggest that an LP can absorb a meaningful portion of the available co- investment capital, which is a critical factor since GPs typically aim to limit the total number of participants in a single transaction. Furthermore, GPs are inclined to contact LPs who have a proven track record of interest or prior participation in such deals.

Efficiency and certainty are highly valued by GPs, who require co-investors capable of responding promptly and reliably. Consequently, GPs favor LPs with a defined internal review process, which allows for a quicker determination of interest to successfully syndicate the deal. While many managers prioritize LPs with these capabilities, others may offer opportunities more broadly across their entire investor base.

The Co-investment Universe

Co-investment fundraising has generally trended upward over the last decade, reaching a historical high for private equity co-investing in 2021. This period of expansion occurred alongside the most robust annual fundraising for traditional private equity in over twenty years.

Figure 2. Global Private Equity Co-investment Fundraising

Source: Pitchbook, as of March 30, 2023. Note, this is based on fundraising activity tracked by Pitchbook and may understate total co-investment fundraising.

LP Sentiment

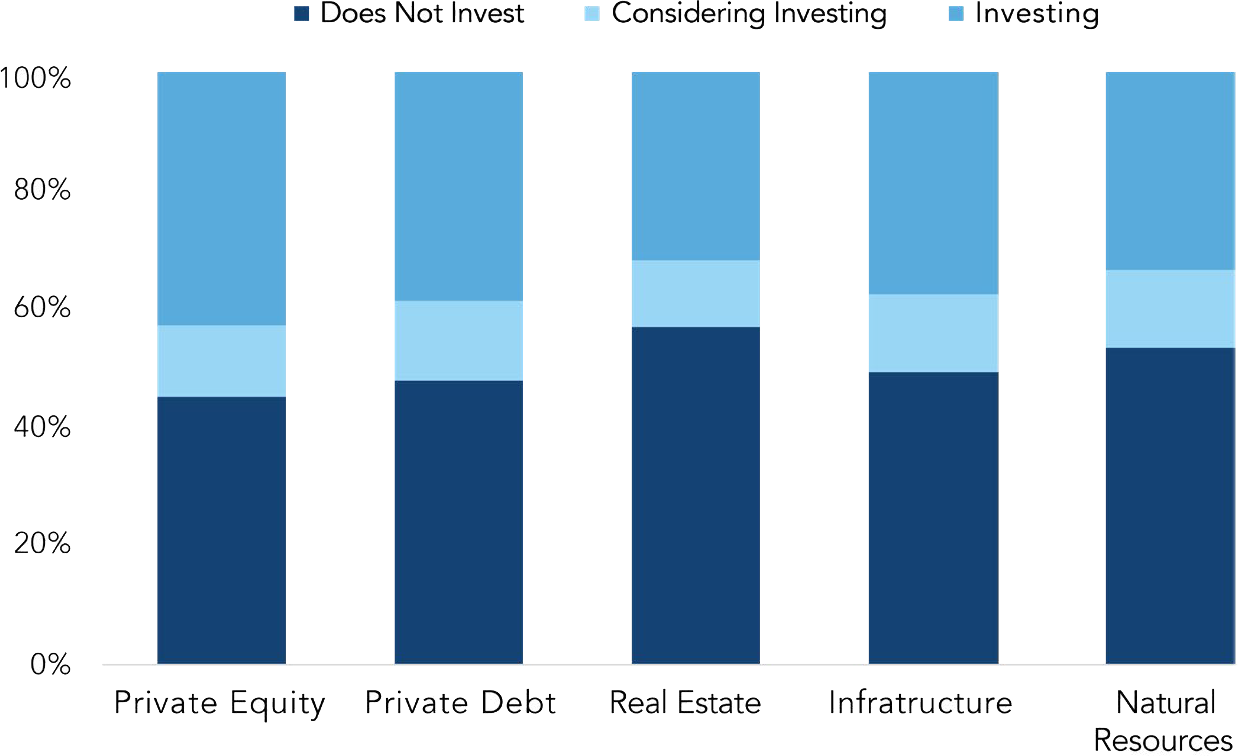

Co-investments span the diverse array of private market strategies supported by institutional investors, including private equity, private credit, infrastructure, real estate, and natural resources. Recent survey data (shown in Figure 3) indicates that private equity continues to hold the highest proportion of investors who are currently active or actively exploring co-investment opportunities, followed closely by private debt and infrastructure.

Figure 3. LP Participation in Co-investments by Asset Class

Source: Preqin Fund Terms Advisor 2024, as of June 30, 2024.

Unsurprisingly, the larger an LP’s allocation to private equity, the more likely it is that they will participate in co-investments (see Figure 4). This correlation is to be expected, as co-investments require additional capital, due diligence, and monitoring, all of which are more likely to be present in a larger private markets program. Larger LPs are also likely to have assembled a deeper stable of GPs from which to source co- investment opportunities, in addition to building an internal team for evaluating them.

Figure 4. LP Participation in Private Equity Co-investments by Current Private Equity Allocation

Source: Preqin Fund Terms Advisor 2024, as of June 30, 2024.

The Co-investor’s Perspective: Benefits to the Co-investor (the LP)

A key feature of co-investments is access to lower fees or avoiding certain costs altogether. Unlike traditional fund commitments, which typically charge a management fee (e.g., 2% annually) and carried interest (e.g., 20% of profits), co-investments often charge little to no management fee or carry. This reduced fee structure can make a meaningful difference by contributing directly to higher net returns for the investor.

Co-investments may also offer enhanced control over portfolio exposures. Investors in a blind-pool fund are required to participate in every underlying investment the fund makes. Alternatively, co-investing provides LPs with the flexibility to customize their portfolio by increasing participation in transactions, aligning better with their specific objectives. The ability to perform target-specific due diligence allows the co-investor to tailor their exposure to particular strategies, industries, and geographies of interest.

Co-investing can further allow for a more rapid deployment of capital, helping to mitigate the J-curve. In a traditional private markets fund, capital is typically drawn down over a multi-year period following the initial commitment. This leads to an early period where fees are incurred while capital is only partially deployed, resulting in negative returns before distributions begin. This phenomenon is known as the J-curve. Because co-investment capital is deployed immediately into an active deal, it can help offset this effect.

By being a regular and reliable participant in co-investments, an LP can strengthen its relationship with the GP. Such a bond can be particularly valuable when dealing with GPs whose funds are frequently oversubscribed. Additionally, co-investments provide an opportunity to increase exposure in highconviction deals while allowing the LP’s internal team to develop expertise in vetting opportunities. Co-investments may also serve as a training ground for staff in deal sourcing, screening, underwriting, and monitoring, often providing an essential first step toward a full direct equity investment program.

Considerations for the Co-investor

Co-investments present additional considerations for LPs beyond those associated with traditional investments in a private markets fund. A primary concern for co-investors is whether the opportunities offered are of lower quality than those retained exclusively for the fund, where the GP would earn full carried interest. This raises the question of whether GPs engage in “adverse selection.” However, comprehensive research comparing the returns of co-investment transactions against those held solely by a fund shows no meaningful difference in average gross performance. Regardless of these findings, investors should always consider the potential for this moral hazard.

While some co-investments are syndicated after a transaction is finalized, most occur simultaneously with the GP’s investment. Consequently, the window between an LP being shown a deal and the required approval is often very short. Maintaining efficient, streamlined internal review and approval processes is essential for meeting these condensed deadlines. To manage these complexities, some institutional investors delegate discretionary authority for co-investment decisions to their investment staff. This authority is typically governed by specific guidelines, such as maximum investment limits per deal or restrictions on certain industries and geographies.

By co-investing, an LP essentially invests twice in a specific company or asset. In many cases, the size of the co-investment significantly exceeds the stake held through the fund investment. This leads to a higher concentration risk than an investor would typically face in a commingled fund, potentially resulting in a less diversified portfolio and an increased risk of loss. Such risk may be mitigated if an LP builds a diversified co- investment portfolio or invests in a dedicated co-investment fund to achieve broader exposure.

Finally, co-investments often carry a bias toward larger deals and companies, as these transactions frequently require the additional capital co-investors provide. This can also lead to headline risk, as a co- investor may be more easily identified with a specific, high-profile investment.

The GP’s Perspective

Benefits to the GP

GPs typically offer co-investments for several strategic reasons, most fundamentally when a potential investment is too large for the fund to absorb alone. Utilizing a co-investment structure allows a GP to pursue attractive, high-capital opportunities that would otherwise be unfeasible. This expansion of available capital also helps the GP maintain unilateral control over the investment, avoiding the need to form a consortium with other GPs or financial sponsors.

Additionally, co-investing can help reduce portfolio risk. By inviting LPs to provide supplemental capital, a GP can limit the fund’s exposure to a single large asset. This allows for a more even distribution of risk across the portfolio and ensures adherence to concentration limits while still participating in high- conviction deals.

Finally, co-investments serve as a powerful marketing and loyalty tool. Offering these opportunities helps attract new investors and deepens existing relationships. This long-term focus on relationship-building and future fundraising often outweighs the incentive to offer “inferior” deals, mitigating concerns regarding adverse selection.

Considerations for the GP

Co-investments also introduce unique challenges for GPs. A primary risk is the potential loss of unilateral control, which can lead to the dilution of rights in more active structures. Furthermore, GPs must dedicate significant time and costs to managing co-investor due diligence requests and negotiating investment terms. There are also increased ongoing management and reporting requirements to satisfy co-investor needs. Lastly, while co-investments can strengthen bonds, they also carry relationship risk; an unsuccessful co-investment could potentially damage a long-standing partnership with an LP.

How Have Co-investments Performed?

Unlike the broader private equity fund universe, there is no comprehensive database for co-investments. Consequently, investors must rely on independent academic studies, which, while comprehensive, often lack the most recent data. These can be supplemented by examining the published track records of long- term institutional co-investors, though such data is more anecdotal and subject to idiosyncratic risks.

Because co-investments are offered with more attractive economics, their net performance is expected to be higher than traditional fund investments if gross performance remains equal. Most investors pursue co- investments not necessarily in search of superior “alpha” at the deal level (favorable selection), but rather to capture the same gross returns as their fund investments while benefiting from a higher net return due to lower fees.

Ways to Access Co-investments

Investors have several ways that they may be able to access co-investments, the most common of which are listed below, along with some of their key benefits and considerations.

Partnering with Existing GPs

Private market investors who have established mature portfolios often hold interests in a wide variety of funds, allowing them to develop long- standing relationships with their GPs. Through these partnerships, the LP gains deep familiarity with their management team, core strategy, and investment track record. Because of this history, the LP typically feels they have already performed significant due diligence on the manager itself. However, while the relationship is established, rigorous due diligence is still required for each individual co-investment opportunity. Additionally, LPs may be able to leverage the size of their existing fund commitments to negotiate more favorable fee structures for these specific direct investments.

Investing in a Dedicated Co-investment Fund

In this structure, the LP delegates full responsibility and discretion for sourcing, vetting, and portfolio construction to a specialized fund manager. While the manager handles the underlying asset selection, the LP is still responsible for vetting and selecting the appropriate fund manager. It is important to note that this structure typically involves an additional layer of fees paid to the co- investment fund manager, which may partially offset the economic benefits traditionally associated with direct co-investing.

Partnering with GPs Outside the Portfolio (One-off Transactions)

To broaden the landscape of potential opportunities, a private market investor may pursue co-investments with General Partners in whose current fund they do not hold an interest. While this approach significantly expands the pool of available deals, it typically requires a more intensive workload. Because there is no existing partnership, the LP must perform comprehensive due diligence on both the investment manager and the specific underlying asset. Furthermore, in these one-off transactions, the LP generally possesses less leverage for fee negotiations compared to their status as a core fund investor. Despite these hurdles, the strategy remains a valuable method for institutional investors to access specific sectors or high-conviction deals that fall outside their existing GP network.

Utilizing Third-Party Intermediaries

If an LP lacks the established relationships or internal resources to build and monitor a co-investment program independently, they can hire a third-party intermediary. These specialists typically possess a vast network of GP relationships and significant experience in evaluating direct deals, effectively acting as an extension of the LP’s team. In this arrangement, the LP may choose to retain discretion over individual investment decisions or delegate that authority to the intermediary. While the LP must still vet, select, and monitor the intermediary, the structure allows them to clearly define investment preferences, sensitivities, and veto rights. Similar to a dedicated fund, this model involves an additional layer of fees paid to the intermediary, which must be weighed against the benefits of expert sourcing and execution.

Structuring a Co-Investment Program

Just as with traditional fund commitments, the cornerstone of a successful co-investment strategy is investment alongside skilled private market fund managers. Investors must look beyond the individual deal to evaluate the manager’s institutional depth, historical strategy, and ability to drive value. In many cases, the GP’s operational expertise is as decisive a factor in the investment’s success as the company’s own financial fundamentals.

To build a durable program, LPs should integrate several core structural pillars:

Sourcing – For investors with constrained resources or limited capacity to actively originate deals, the most effective strategy is to rely on their most sophisticated fund managers to provide transaction flow. Success in this model requires the investor to be highly transparent with their GPs regarding their specific investment criteria, including preferred sectors, transaction sizes, and geographic focus. To increase the investors’ chances of completing their due diligence, they may also encourage fund managers to involve their team in the early underwriting stages of any potential co-investment opportunity.

Fully vetted fund managers – The most efficient path to a co-investment is through managers the LP has already rigorously underwritten and approved. An existing commitment provides the LP with a window into the GP’s internal decision-making and performance consistency. While primary focus should remain on these known quantities, LPs should remain open to high-quality external managers when specific portfolio gaps need to be filled.

Playing to strengths – Risk is best managed by backing a GP when they are operating within their “strike zone.” LPs usually are best served by prioritizing deals that align with a manager’s proven track record in specific industries or geographies.

Investment size – Discipline in check-sizing is vital to avoid unintended concentration. Investment limits should be defined in the Investment Policy Statement. A common safeguard, particularly for newer programs, is to cap the co-investment amount at a conservative fraction of the capital committed to the manager’s primary fund.

Co-investment structure – To maintain a clean alignment of interests between the investor and the fund manager, co-investments should be executed in the same securities, at the same time, and under identical terms, preventing any potential conflicts of interest regarding the capital structure.

Underwriting process – To maximize efficiency and decision-making flexibility while minimizing the time required for investment decisions, investors should utilize a co-investment underwriting process that mirrors the framework already established for fund investments.

Monitoring – Investors should consider implementing a co-investment monitoring program that integrates with their existing fund processes while adding features specific to direct assets. Monitoring should be managed alongside the broader GP relationship, involving ongoing evaluation of both the asset’s performance and the manager’s execution. While most LPs defer to the fund manager for day-to-day management, some may be more actively engaged, occasionally securing a seat on the board of directors. Regardless of board representation, co-investors typically negotiate specific information rights to access board-level documentation.

To track financial strength and the quality of GP interaction, co-investors establish a regular monitoring rhythm, often monthly or quarterly. This is usually supported by a financial information package and direct discussions with the fund manager or company leadership. Using a standardized template allows staff to efficiently summarize investment details, manager commentary, and internal observations into a cohesive reporting framework.

Conclusion

Co-investments offer a unique and advantageous opportunity for limited partners to invest alongside general partners directly into specific portfolio companies. This collaborative structure allows LPs to bypass the “blind pool” risk inherent in traditional private market funds, providing them with greater control and flexibility. By participating in co-investments, LPs can benefit from reduced fee loads, more targeted portfolio exposure, and the potential for enhanced net returns.

However, co-investments involve distinct considerations and risks. LPs must be prepared for compressed decision-making timelines and the requirement for highly efficient internal review processes. There is also the potential for increased concentration risk, as co-investments typically result in more significant exposure to individual assets. Despite these challenges, co-investing can strengthen the bond between LPs and GPs, offering valuable opportunities to enhance investment strategies and gain deeper insights into private markets.

Ultimately, the success of a co-investment program depends on the careful selection of opportunities and the effective management of associated risks. Both LPs and GPs stand to benefit from this approach, with GPs securing additional capital and LPs achieving more customized and potentially lucrative outcomes. Investors looking to build a co-investment portfolio should rigorously assess their internal capabilities and develop the strategy and staffing necessary to maintain a professional program. As the co-investment landscape evolves, it remains a compelling option for investors seeking to optimize their private market portfolios.

Appendix: The Underwriting Process

Co-investment underwriting typically includes several distinct stages, beginning with a clear determination of the investor’s role in the market.

Sourcing

A critical first step in the underwriting process is determining where an investor falls on the spectrum of active versus passive deal sourcing. The general strategies for approaching co-investments are:

Passive follower – Investing in virtually every co-investment opportunity presented by the fund manager.

Selective follower – Choosing co-investments based on an internal assessment of the opportunity’s quality or portfolio fit.

Co-leading – Taking a full leadership position in the investment on an equal basis alongside the fund manager.

Regardless of their position on this spectrum, the investor should work closely with fund managers to identify potential opportunities. Staff must clearly communicate the specific criteria, characteristics, size, and other features that make a co-investment attractive to the institution.

Additionally, the investor’s internal underwriting, decision-making, legal review, and funding processes should be shared transparently with the GP. This ensures the fund manager is fully aware of the LP’s operational requirements and timelines when considering them for a particular co-investment opportunity

Screening

To streamline initial reviews, some co-investors utilize an “investment assessment tool” consisting of specific criteria to provide a transparent and efficient “playing field.” An effective initial screen typically focuses on the following:

Attractive economics – Prioritizing opportunities with low or no management fees and carried interest.

Appropriate size – Ensuring the check is large enough to justify the resource expenditure but small enough to avoid over-concentration in the portfolio.

Portfolio fit – Verifying the investment aligns with the investor’s geographic, industry, and development objectives.

Additional screening factors may include valuation metrics, the caliber of the fund manager, the quality of the underlying management team, and overall investment risk. Investors may also require that the GP secures a board seat or specific information rights as a prerequisite for consideration.

Review Process

The path to a final decision typically involves multiple stages to ensure rigorous oversight. These steps often include an initial “screening,” a “preliminary review” (where resources are officially committed to the deal), and a “final review.”

These reviews are generally conducted by a committee of senior professionals to provide diverse perspectives. Given the accelerated timelines of co-investments, this committee must maintain a flexible meeting schedule to react to unpredictable deal flows.

Due Diligence

The depth of due diligence often depends on the investor’s chosen strategy. For “passive followers,” the approach is typically “top-down,” focusing on the opportunity to deploy more capital with high- conviction managers. Conversely, for “selective followers,” diligence is a time-intensive process requiring a multi-level team. Investors often pair team members who underwrote the GP with specialists in the specific industry or sector.

Due to tight time constraints, identifying key attributes and risks early is critical. Qualitative diligence focuses on the sponsor’s track record, management’s success and succession planning, and the company’s competitive position and growth potential. Quantitatively, LPs employ valuation models that stress-test the GP’s base case across various assumptions, such as margins and exit multiples, while benchmarking the deal against comparable public and private transactions.

Many investors also utilize third-party firms to review co-investments alongside their internal teams. These specialists typically focus on transaction valuation, industry trends, and projected growth. Additional due diligence may cover legal, accounting, insurance, employee benefits, and tax considerations. The findings are synthesized into a report for the LP’s committee as part of the final review. However, integrating third parties can complicate information flow under tight deadlines, leading some investors to establish minimum dollar thresholds for requiring external reviews.

Legal

Co-investment legal documentation differs significantly from fund investments and varies across jurisdictions. Investors must determine the optimal point to involve internal or external legal counsel, balancing the need for thorough protection with the transaction’s rapid timing requirements.

Approval, Closing, & Funding

As co-investments involve multiple review stages, maintaining clear governance is considered best practice. This includes defining rules for majority versus unanimous votes, committee membership, and quorum requirements. Clear protocols must also exist for communicating decisions internally and to the fund manager.

The closing and funding process must be meticulously organized to ensure all documentation is executed and capital is positioned in time for the transaction’s close.

Other Considerations

To ensure the successful implementation of a co-investment platform, LPs must address several critical structural issues. These legal and economic rights are essential for protecting the investor’s interests:

Information rights – Ensuring access to the data necessary to monitor the investment’s health.

Preemptive rights- Providing the ability to invest additional equity to avoid ownership dilution.

Tag-along rights – The right to sell their interest alongside the GP during an exit.

Transfer limitations – Including rights of first refusal to purchase other investors’ interests.

Governance rights – In limited cases, securing a board seat or observer rights, though these require careful consideration of potential fiduciary responsibilities.